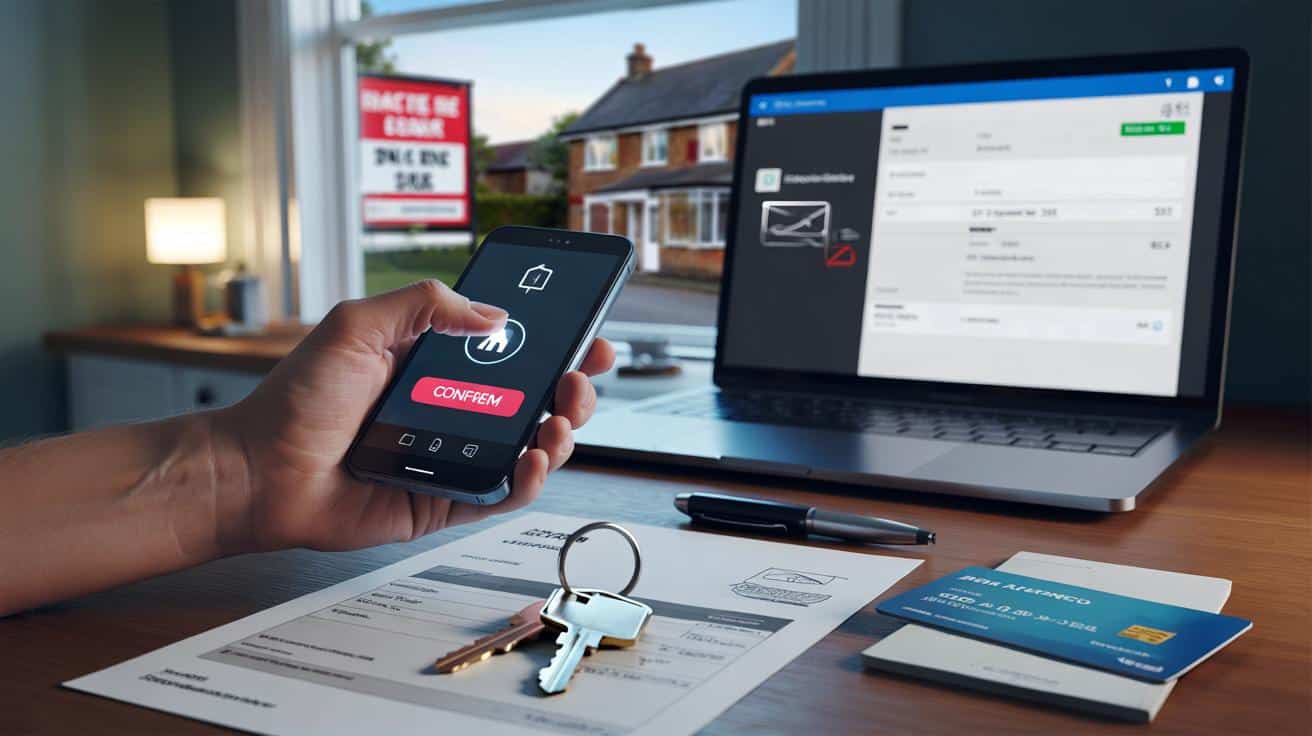

You lined up the paperwork. Then a single email lands, and everything feels suddenly fragile.

Police and fraud specialists warn that a growing email scam targets homebuyers and renters at the point of paying large sums. Criminals piggyback trusted conversations, change one critical detail, and sweep away entire deposits in minutes.

Threat rising across property deals

City of London Police and Action Fraud report a steady rise in payment diversion fraud, often called conveyancing fraud. Offenders infiltrate email threads between buyers and their legal representatives, then send bank details that look legitimate. Victims believe the message comes from their solicitor or estate agent and push funds to the wrong account.

Between April 2024 and March 2025, reported conveyancing losses reached £11.7 million, with an average loss of £78,393 per case.

Most cases relate to residential transactions. The pattern is consistent: a last‑minute email arrives, stresses urgency, and provides “updated” banking details. The tone matches earlier emails. Logos and signatures look right. By the time the buyer realises, the money has been moved through mules and is hard to trace.

Not just home purchases

Fraudsters also target rental deposits and probate payments. Wherever large transfers happen, criminals try to intercept them. They spoof domains, take over compromised accounts, and coach victims through the transfer so it passes bank security checks.

Criminals rely on trust and urgency. Any unexpected bank detail change should trigger a pause and a phone call to verify.

How the scam works

- The setup: attackers monitor or mimic email accounts used by solicitors, agents or clients.

- The switch: they send “updated” client account details or a fresh invoice near completion or tenancy start.

- The transfer: the victim sends the deposit by Faster Payments or CHAPS to the fraudster’s account.

- The aftermath: funds move quickly through mule networks, often offshore, before a recall can bite.

| Period | Reports | Total losses | Residential reports | Residential losses | Average loss |

|---|---|---|---|---|---|

| 1 Apr 2024 – 31 Mar 2025 | 143 | £11.7m | 140 | £10.97m | £78,393 |

Red flags to watch for

- Bank details change at short notice, especially on completion day.

- Emails with tiny domain differences (one letter missing or swapped).

- Pressure to pay quickly or risk losing the property.

- Attachments with bank details that you have not seen confirmed in person or by phone.

- Confirmation of Payee message that does not match the named firm.

Genuine firms rarely change their client account. Treat any change as suspicious until verified on a phone number you already trust.

What to do before sending money

- Pre‑agree payment steps at the start of the transaction, including the bank account details and how they will be confirmed.

- Verify any account details by calling your solicitor or agent on a known number from their letterhead or website. Do not rely on numbers in a new email.

- Use the bank’s Confirmation of Payee check. If it shows a mismatch, stop and call.

- Set a 24‑hour cooling‑off period for large transfers. Ask your bank to raise payment alerts and lower transfer limits temporarily.

- Avoid emailing bank details. Ask for them to be confirmed verbally and sent via a secure portal if available.

- For joint buyers, require two approvals before any transfer leaves your account.

If you think you’ve been duped

- Call your bank immediately and ask for a fraud recall and a trace on the payment.

- Contact the firm you meant to pay. Their rapid notice to their bank can help freeze mule accounts.

- Report to Action Fraud and obtain a crime reference number. Inform your conveyancer and estate agent.

- Preserve evidence: emails, headers, invoices, and any messages or call logs.

- If a solicitor’s identity was used, notify the relevant regulator so they can warn others.

Speed matters. The first hour after a transfer is critical for chasing and freezing funds.

Will you get your money back?

From late 2024, reimbursement rules for authorised push payment fraud strengthened across Faster Payments. Outcomes still vary by circumstances and the payment type. Large property transfers often move via CHAPS, which sits outside those reimbursement rules. That means recovery can be difficult. Some buyers hold specific insurance or receive partial help where professional negligence applies, but this is not guaranteed. Assume you will need to protect yourself up front.

A real‑world scenario

A couple had exchanged contracts and were preparing to send their deposit. An email arrived that perfectly matched the existing thread. The sender’s address differed by a single missing letter. The message asked for 10% of the purchase price and attached a document with the firm’s logo and “client account” details. The pair transferred the first tranche, then the balance. Only later, when the real solicitor confirmed no money had arrived, did they notice the subtle domain change. By then, the funds had moved across several mule accounts.

Practical ways to harden your transaction

- Insist on a “payment rehearsal” call one week before completion to confirm the exact account name and sort code.

- Ask your solicitor to confirm, in writing at the outset, that their banking details will never change by email.

- Use secure client portals with two‑factor authentication rather than relying on email for sensitive documents.

- Request a paper letter with bank details sent to your home address, then verify by phone before use.

- Keep one device (a tablet or spare phone) for property matters only, reducing the chance of malware capturing your messages.

Why the average loss is so high

The average case involves a deposit close to 10% of the purchase price. On a £780,000 London flat, that deposit is £78,000. For many households, that equals roughly three years of take‑home pay for a median earner. Losing that sum can collapse the chain, trigger extra fees, and erode mortgage offers tied to specific timelines.

Make a quick personal risk check

- List everyone who will email you during the move. Store their verified phone numbers now.

- Decide a maximum you will send in one go without an in‑person or video confirmation.

- Set a rule: no new bank details accepted within 72 hours of completion without a confirmation call to a known number.

- Ask your bank about dedicated support for large transfers and how to escalate a recall within minutes.

One extra phone call can be the difference between keeping a £78,000 deposit and watching it disappear.

Key terms that help you talk to your bank

- Authorised push payment fraud: when you are tricked into sending money to a criminal.

- Confirmation of Payee: a name‑checking service that warns when the account name does not match.

- Payment recall/trace: the urgent request your bank sends to freeze funds at the receiving end.

- CHAPS vs Faster Payments: large, same‑day CHAPS transfers may not fall under the same reimbursement rules as Faster Payments.

If you are close to completion or starting a tenancy, agree verification steps today. Share them with your conveyancer, your agent, and anyone else who might email about money. Criminals want you rushed and distracted. Slow the process at the point of payment, and you keep control of your £78,000.

Terrifying. I’m definately adding a 24-hour cooling-off rule and phone verification for any transfer over £1k.